how to find the perimeter of a square

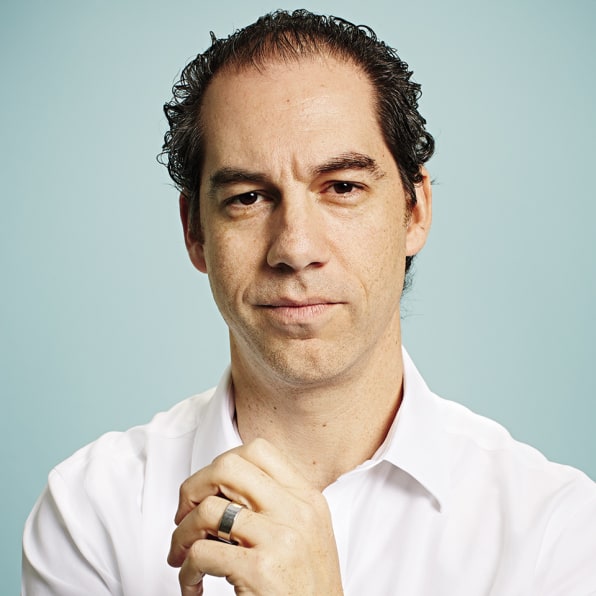

Jack Dorsey doesn't know how to grade his performance. It's early May, and Dorsey has just finished his annual reviews of Square's 800 employees. He now needs to complete his own. So the Square CEO sends out a Google Doc to the entire company soliciting feedback, but he makes two suggestions that border on the masochistic: All comments should be anonymous, and all comments should be visible to everyone inside the company. "Write whatever you want," Dorsey tells his troops, adding that he wants to learn "where I've done well, where I've done poorly, and where I've completely screwed things up."

When we meet for a walk on a gray morning in San Francisco several weeks later, Dorsey is in great spirits. He jokes about overly cautious Californians who refuse to jaywalk; and in the elevator when we bump into two police officers leaving Square headquarters, Dorsey greets them with a smile and a handshake befitting a small-town mayor. He tells me he hasn't read through all the feedback yet from his Square colleagues–he received more than 500 responses–and will only hint that much of it stressed the need for more "focus" at the company. He's being intentionally vague, of course. When I ask what grade he'll give himself in the self-assessment he's writing, Dorsey tersely replies, "Not an F."

How about a C, then–or even a C-minus? Square is no longer the high-flying startup it once was. When Twitter cofounder Dorsey launched the company in 2010, pundits heralded its potential to upend the stagnant payments space. The startup had developed a novel credit- and debit-card reader, which could attach to mobile devices and let merchants accept payments virtually anywhere. The company also launched a promising digital-wallet app, which enabled customers to link their bank cards with their phones to purchase goods–no more need for plastic or paper. To an adoring press, Square had an Apple-like flair for design and seemed destined to revolutionize any number of business domains: data, e-commerce, social, deals. By early 2014, investors had plunged $340 million into the startup, which was valued at $5 billion.

Since then, the mood has soured. Nick Bilton's insider tale, Hatching Twitter, painted an unflattering portrait of Dorsey as a backstabbing egotist who took more credit for Twitter's success than he deserved. Not long after, reports surfaced that Square had delayed its IPO due to revenue troubles. Then a scathing piece in The Wall Street Journal depicted Square as a company desperately searching for an exit after losing $100 million last year. The problem? Square's core business, processing transactions and taking a tiny cut for the effort, was simply not all that profitable. To put a finer point on it, venture capitalist Fred Wilson recently penned a blog post suggesting that Square would soon have to make "some hard choices."

The coming months for Square will be pivotal. As it burns through cash, the company must create new sources of revenue to justify its high valuation; in the process, it will try to prove that it can create a hugely profitable business as well as a transformative one. Contrary to some of the most dire predictions, Square isn't going bankrupt tomorrow. But in a culture where failing fast is a badge of honor, and where every startup–no matter how banal–aims to change the world (an ambition so cliché it was recently parodied on HBO's Silicon Valley, which Dorsey claims he's never seen), the idea of building a business that's merely sustainable, rather than revolutionary, may seem worse than a flameout. Square has done an enormous number of things right; what's more, it has overcome an extraordinary number of hurdles just to get to this point. And yet, Dorsey admits his team now faces "existential questions" about Square's future.

Next to the graveyard of overhyped startups, there is a purgatory where companies like Groupon and Zynga toil–successful but not relevant, almost (or barely) profitable yet inconsequential. These are firms that, despite their promise, were never quite able to escape the clutches of mediocrity. Does Square now face the same fate?

As if to prove he and his company will never willingly accept middling success, Dorsey and Square have spent the past 12 months in a frenzy. The company has embarked on an aggressive effort to digitize more and more aspects of our financial lives–peer-to-peer money transfers, cash loans, enterprise software, online markets, ordering. It's a risky strategy that has positioned the company not only against Google and eBay's PayPal, but also against Amazon, Etsy, GrubHub, Yelp, and a slew of traditional financial players. Finance is arguably the last unconquered industry of Silicon Valley. "With any challenge," Dorsey says, "there's a fight-or-flight psychological reaction: You either continue to fight, or you go away." Obviously, he's chosen to fight.

For a company that deals with obscure financial intermediaries and wonky regulatory issues, Dorsey has already done the difficult work of getting customers to feel passionate about Square. His talents are not so much in hard-core engineering–like, say, Elon Musk's–than in conceptualization and design. Dorsey is the kind of guy who can say, without irony, that invoices are "sexy"–and actually sound convincing. Or he's the kind of guy who will ask his developers to alter at the last moment the screen color of an app–as he did recently for a new product called Square Cash–from aqua to brilliant green. "Jack came in and was like, 'I don't like this green–it's not happy enough,' " recalls product lead Brian Grassadonia. "We were like, 'What the hell are you talking about?' " The different hue Dorsey chose, Grassadonia says, at first looked "horrible, and reminded me of sickness." But soon, he adds, "I really came to love it. It's perfect."

If you take a look at the app, it actually does look close to perfect. It's a good example of how Dorsey's aesthetic discernment and marketing savvy catapulted Square past its competitors in the early days. And yet, it's these same gifts of Dorsey's that have masked more subtle problems plaguing Square.

Without question, Dorsey and cofounder Jim McKelvey deserve credit for ripping through the complexity of commercial transactions: Square Reader, their minimalist device for swiping credit cards that plugged into phones via audio port, was a masterstroke of simplicity, as was the company's then-unique model of charging merchants a flat 2.75% rate per transaction, an approach that untangled the industry's antiquated cost structure (with all its hidden fees). These innovations opened Square up to a massive, growing industry of micromerchants–baristas, florists, food-truck owners–who flocked to the service. By late 2011, the company was processing $1 billion in payments on an annualized basis; a year later, not long after the company launched Register–software that transforms an iPad into a point-of-sale terminal–its annual payments volume had ballooned to $10 billion. Investors climbed aboard. In August 2012, when Starbucks invested $25 million in Square as part of a $200 million round valuing the company at $3.25 billion, Square was chosen to process all credit transactions done at 7,000 branches of the coffee chain's U.S. stores. Starbucks CEO Howard Schultz proclaimed Square was "the fastest-growing opportunity we've ever seen in terms of customer acceptance."

Square's earnings told a different story. Making money from payments processing is a bit like building a business by selling soda simply for the bottle deposit: It takes a lot of effort just to convert a $1 bottle of Coke into a nickel return, and only in extreme bulk can those nickels start to add up. More troubling, with Square's business, the majority of those nickels go to the financial intermediaries it works with. At every swipe, Square takes its small cut of the transaction price, but 70% (or more) of that fee often goes to Visa, MasterCard, and other institutions that handle risk and fraud detection, as well as card-member rewards and services. With higher-end American Express cards, Square even loses money on charges. "If your business model is based on making pennies from transactions, you're in trouble," says a former top executive at one of the big card networks who has worked closely with Square.

The payments data that Square collects in the process are extremely valuable–tracking who purchased what, when, and where. At an individual store level, this data can show hot-ticket items, customer loyalty, and employee output; in aggregate, it can provide useful analytics, like, say, the average price of dessert in lower Manhattan versus Williamsburg, Brooklyn. Even so, Square's only route to profitability in the near term was through achieving mass scale. "The reality is, popping a reader onto your phone and swiping a credit card is a razor-thin-margin business," says Anuj Nayar, a senior director at PayPal, which, despite offering the same technology as Square and processing more mobile-payments volume in 2012, was seen as a dying incumbent. (Nayar chalks up the negative sentiment around PayPal to the "Jack Dorsey bubble" inflating Square's potential.)

Dorsey understood payments processing couldn't be the endgame. "We always knew it was not our core business," he says. "We knew the real business was around the data." Indeed, Dorsey outlined some of these ambitions in his first pitch to investors. Yet the company demonstrated little capacity to evolve beyond payment processing. Part of the reason was a lack of direction inside the company and a crippling organizational chaos, according to a string of former employees. As the company tried to keep pace with its rapid growth, Square's leadership seemed unable to execute on new product ideas. It also wasn't sure who it should create products for. "We started having conversations like, 'Should we put more emphasis on the seller side or the buyer side?' " Dorsey recalls. "It became seller versus buyer, and we kind of lost sight of the connection between them."

The fuzzy focus culminated in Square Wallet, which was initially called Card Case. Though Dorsey won't acknowledge it publicly, the aim internally, says one source, was to "own both sides of the counter"–vendor and customer–so the company could one day "cut out the credit-card companies altogether." (At weekly all-hands meetings, former COO Keith Rabois, only half-jokingly, used to announce the projected date on which Square's payments-processing volume would overtake Visa's.) Instead of helping consumers pay with their phones, like many other digital-wallet products, Square's Wallet app enabled consumers to open a virtual tab with a nearby shop and then pay for items merely by saying their name when they arrived. Despite its popularity with the tech vanguard, Wallet saw barely any adoption. Few merchants accepted it, partly because few consumers paid with it, and vice versa. Even where Square Wallet was accepted, cashiers often didn't know how it worked. "It wasn't necessarily faster, or more convenient," Dorsey says, looking back. "It felt more futuristic, but that doesn't make it better."

One of the main reasons for the Square-Starbucks alliance was to bolster Wallet at the coffee chain's U.S. stores. But to lock in the deal, say insiders, Square had to agree to a substantially different payment structure with Starbucks, whether charged payments were done with Wallet or not. The effect was to all but eliminate Square's margin. As outsiders praised the partnership, Square executives knew what was coming: The following year, the company would lose $25 million from Starbucks transaction costs alone (and will continue to incur losses until the contract expires next year). Essentially, Square executives saw the gambit as a marketing expense for Square as well as for Wallet. "All I will say is there was a plan, a conscious decision to do the Starbucks deal, and we decided to place that bet–obviously nobody forced us to do it," says Square investor Vinod Khosla, defensively. To him, Wallet wasn't a bad product, it just came too soon. "Square's payment volume was task one–that's all Jack should've talked about. You can't reach step five before you build steps one, two, three, and four."

With Square's payment volume reportedly on track to hit $20 billion by the end of 2013, Dorsey continued to garner lavish praise, gracing the covers of magazines (including this one), teasing that he may one day run for mayor of New York City, and joining the board of Disney. By the year's end, Dorsey appeared in a glowing 60 Minutes profile, where he wowed reporter Lara Logan with Square Wallet. Logan began the segment by saying, "When Jack Dorsey invented Twitter, he changed the way we communicate. Will his company Square change the way we shop?" Dorsey's ambitions and utterances at almost every turn assured the crowd that his company would be revelatory. Even when Wallet was struggling in the market, some colleagues say that Dorsey would gloss over the weak numbers internally.

And yet, here's the thing: Square's business is not a bad one. It's just not nearly the supernova it was made out to be. Despite the recent wave of negative press, Square continues to expand. Payment volume, excluding the disastrous Starbucks deal, grew more than 350% in the past two years and will reportedly reach around $300 million this year in gross profit. While the company is still incurring heavy losses, Square executives make a convincing case, backed up by internal company documents, that this is mostly by choice. It's investing significantly in hiring, marketing, and new products. If it didn't, Square could be a profitable company. "The rumors of our demise have been greatly exaggerated," says CFO Sarah Friar.

While Square has indeed made preparations for a potential IPO, company executives also insist that many published details about a public offering or a potential acquisition were incorrect. One board member goes so far as to argue that the stories were planted by a competitor or someone with an ax to grind, while Dorsey simply finds the narrative boring. ("There's a buildup phase, then a takedown phase. Facebook, Google, and Apple all got it; Twitter is getting it, and Square is going to get it, too. Who cares?") And while Square employees will tell you Dorsey's vision hasn't changed despite Square's stumbles, they admit the company's focus has moved, finally, beyond payments. After all, it must: Plan B is the only option for a viable future. (Square takes issue with Fast Company calling the move beyond payments a "Plan B.")

Tellingly, the visionary now leading the charge isn't Dorsey, but Gokul Rajaram, a 39-year-old product engineer who carries his smartphone in his shirt's chest pocket and exudes a nerdy affection for data. When Rajaram joined Square from Facebook in July 2013, he set out to interview employees from every part of the company to find out what needed fixing. The verdict was predictable: "We were doing a great job building a bunch of features on the payments side of the business," he says. "But we needed to be more aggressive and accelerate building products on top of the payments data." Some teams were inching toward this goal before Rajaram arrived, but he found the efforts "nebulous." After an all-hands meeting in August, he outlined what areas Square would (and wouldn't) work on. As the company kicked into overdrive, Wallet was discontinued.

In a sense, the company has taken a step away from Dorsey, who has kept a lower profile as of late. The company is now pushing the idea that there are "multiple visionaries" at Square today. "There's not a singular force," Dorsey tells me over coffee. "I've told the company multiple times, if I have to make a decision, we have an organizational failure."

Many colleagues, at least, say Rajaram's push was liberating. Whereas before, most teams were developing feature after feature for Square Register, Rajaram reorganized the company into smaller teams to create specific, stand-alone products that can generate profit. They were each tasked with a narrow mission (e.g. "go make receipts a compelling platform") and given a large degree of freedom. Rajaram says self-empowerment is how the ailing Wallet project got killed: Most of the engineers migrated to more exciting products like Order, a new service that lets customers order ahead at restaurants, and nobody wanted to work on it anymore. "The teams made the call," he says. (A Square spokesperson disputes this characterization of Wallet's demise, saying, "The Order app is an evolution of Wallet. We wanted to take what we were doing with Wallet–merchant discovery, menu items, payment–and apply it to Order.") Signs of a renewed sense of purpose are evident all around Square's offices, and a mock movie poster sitting near Rajaram's team captures the ambition: SQUARE QUEST IV: THE SEARCH FOR NON-PAYMENTS REVENUE.

There's need for the urgency. Square's Reader and Register products are no longer unique; a slew of upstarts and big rivals such as PayPal, NCR, and VeriFone now offer their own equivalent iPad systems, which threaten to eat away at Square's merchant share and payments business. "Payments is a commodity game," says Brad Smith, CEO of Intuit, which initially sought to own the space before concluding the margins were too low and the competition too crowded. "Square is in a transition phase and adding components: They're going to have to do more magical things for small businesses than simply accept electronic payments."

And there may be a finite period to pull off this transition. For decades, credit-card companies have thrived off the high processing fees they charge merchants. "It's complete bullshit," says PayPal cofounder (and Square investor) Max Levchin. Due to regulation and new payment alternatives like bitcoin, many industry sources I spoke with agree that transaction fees would significantly decline over time. The card networks are under immense pressure–from retailers and legislators, among other entities–to lower processing rates, which they've long (and vaguely) justified by citing fraud and risk liabilities, while providing scant transparency into how the system actually works. The EU recently proposed a plan to cap credit-card processing fees at just 0.3% of the transaction value, while a 2010 U.S. law curbed debit-card rates.

"They will go away," predicts Levchin of the high fees, adding that Square must find other revenue streams before that happens.

Restaurante 9 is a new eatery on Market Street in San Francisco that serves a summer gazpacho with baby herbs. At lunch, when I arrive, the restaurant is filled to capacity. This is odd: The food is mediocre, the service slow, and the decor lacking. Yet the diners couldn't appear happier. That's because Restaurante 9 isn't a real restaurant; it's a pop-up test kitchen in a conference room on the ninth floor of Square's headquarters. The team is running a full-service lunch to work out kinks in its new product, Open Tickets, a software tool for sit-down restaurants. ("Hi! I'm the product manager, but today I'll be your hostess!" a chipper Square employee tells me before racing off to the kitchen.) In the back room, chalkboards list missing features, such as inputs for seating changes, order cancellations, and peanut allergies. Save for the iPads that the waitstaff use, there's little evidence that Restaurante 9 even utilizes Square. Orders are delivered to the kitchen via printer, and when the check arrives, it includes only a paper receipt.

Not long ago, to improve communication between waiters and chefs, Square might have come up with a digital-only solution. But the company seems to realize that a cook with marinara-covered fingers doesn't want to fiddle with an iPad during dinner rush. Another sign Square is learning from past mistakes: In early 2014, the company started a customer-support phone line. Before, the company believed it could make its products so streamlined that no phone assistance would be necessary, an astonishing (but not uncommon) Silicon Valley notion. After years of complaints, Square relented. Dorsey recently spent several hours manning the phones and was surprised to discover inquiries often weren't about Square–they were about how to set up an iPhone or use iTunes, a stark reminder that Square's clients might not be so tech savvy.

Open Tickets is just one part of a forthcoming suite of services to help merchants in the retail, restaurant, and service industries. Rajaram likes to say Square has now entered "harvesting mode"–the company boasts around 1 million merchants already using Square Register, so he insists it's not a stretch to imagine that Square can up-sell them on incremental (and higher-margin) services, like invoicing and inventory tools. The Square team hints at other future products, including tools for loyalty points, rewards, and marketing. In the meantime, Rajaram is expanding on the launch of a product known as Square Capital, a cash-advance program. Because it has perfect visibility into merchant sales, Square doesn't mind loaning, say, $10,000 to sellers (often overnight) in exchange for a slice of future sales until the debt is repaid. Reception to the pilot was immensely positive, which is why the company is seriously ramping up the program. (Square has a $225 million line of credit, which is partly used to fund Capital.)

Where could the company venture next? Square hardware lead Jesse Dorogusker argues that merchants need help with everything from "delivering arugula to keeping the lights on to upgrading their Comcast Internet." Even redesigning age-old paper receipts is on the docket. ("It takes you five minutes to find the date! It's like finding the expiration date on yogurt!") More hardware is also coming, including a new Square Reader. And multiple sources have indicated a Square credit card has been prototyped–a card that's all black, which some employees have been carrying around in their wallets over the past year. When I press Dorogusker about it, he says, "We're always searching for something better. I definitely won't deny it, but I definitely won't announce anything."

Square later tells me it will not actually be launching a credit card. But it's unclear whether merchants and consumers are interested in adopting any of its other tools–or whether the tools will connect together in a coherent way. Roughly 20% of users of Square Market, the company's online storefront product, have never used Square Register. When the company was deciding how to promote Order, according to design director Paco Viñoly, "we wondered, should it even say Square on it? Should it even have our logo?" And as Rajaram describes the various "buckets" Square will go after, I struggle to take it all in. "We want to be the central operating system of your business," Rajaram says. It's a catchy tagline, but what that means in the real world remains a puzzle.

In fact, ticking through the list of products that Square is launching–Market, Cash, Feedback, Invoices, Order, Open Tickets, Capital, Dashboard, Appointments–makes it easy to wonder whether the company is in panic mode. It's probably more precise to say that Square is scrambling, or that it's hustling. "If you ask me, was Square [Capital] on the agenda four years ago? No. But that's learning," says Khosla. "A year and a half ago, would I have said Order was a big business? No." Also, it may not matter whether all these products work in unison yet, given Square's see-what-sticks approach. "Are we going to nail every single thing we're endeavoring to do now?" says Roelof Botha, a Square investor. "Of course not. If you're batting a thousand in this business, you're not pushing hard enough."

For now, Friar, the CFO, stresses that the company has enough breathing room to experiment. For example, Square Cash allows consumers to exchange money for free through an email or via an app. It doesn't quite fit into Square's merchant-centric products, and the company loses money (often in the range of 25 cents) on every transfer. Still Friar is encouraged. "We gave [the team] a bunch of cash and said, 'You can't lose more than X; go see what you can do,' " Friar recalls. In just eight months, Friar boasts that Cash is already one of the largest peer-to-peer players in the world; it could easily help users, say, move cash from country to country, a money-transfer system that's long been a highly lucrative business for Western Union. "With most of these new businesses," she adds, "we only start funding them and putting a lot of effort behind them if we believe that over the next three-plus years, they can be $100 million businesses."

Recently, Jack Dorsey grew a beard. A scruffy one, with wisps of ginger and gray. It's not the beard one would grow after a divorce, or a tragic loss, or a midlife crisis, but a beard of style. With Dorsey's celery-slight frame and button-down shirt, the beard makes him resemble a hipster farmer. It's this crafted persona, this self-styled meld of artist and entrepreneur, that prompts board member Larry Summers to tell me that with Dorsey's "commitment to design and creativity, he may be as close to Steve Jobs as anybody who is alive today."

It's true that in a certain light, the parallels to Jobs are unmistakable–in Dorsey's ouster from his first company, and in his triumphant return with Square. Yet Dorsey's degree of success, at least so far, makes the comparison an unflattering one; he would have to grow Square into a global, transformational business, just like Jobs did with Apple and Pixar, for it to be otherwise. "If Square succeeds, they'll be this massively valuable [company] unified around payments," says a CEO at another hot commerce startup. "And if they fail, they'll probably have to go through this painful course correction to becoming a small but not insignificant payments company. They won't implode, but it will be painful."

Only in Silicon Valley, perhaps, could success seem so unpleasant; anywhere else, building a minor but sustainable business would be a rare achievement. And yet, Dorsey has always shared the Valley's view of the world. "Mediocrity is not on the agenda for Jack and company; thinking big is the order of the day over there, to a fault," says one former employee, who cites Dorsey's so-called 5,000-year plan for Square, which Dorsey often talks up with his team, despite its absurdity. "I don't think the plan is ever to settle for being a quiet, back-end [service]–he wants to create a company that's as influential as Apple." This may prove to be Dorsey's greatest mistake. In giving him a grade for his performance, you could argue he should have rolled out additional products sooner, or that he should not have set expectations so high with the press and the public. But perhaps his greatest challenge will be coming to grips with the possibility that Square could end up as an enterprise that brings real (albeit incremental) value to the world but never has the revolutionary impact of Dorsey's first startup, Twitter.

Dorsey is well aware of the stakes. Outside a café on a quiet side street in the Hayes Valley neighborhood of San Francisco, he sips a cappuccino as a gentle breeze sways the purple flowers behind him and a bird chirps by his feet. "It goes back to that fight-or-flight idea," Dorsey says. "Some people are like, 'I love that challenge–wow, it scares me, but I'm in.' And some people are like, 'Ah, nope, I'm doing a photo startup.' " There's no question that Dorsey is in the first camp. But when I ask whether he'll be remembered more for Twitter or Square, Dorsey shakes his head. "I don't care. I honestly don't care!" he says, laughing. He remarks that he focuses instead on building "something that resonates with everyone on the planet–then you're really understanding humanity, and that's what I personally want to feel."

If Square actually begins to resonate with everyone on the planet, that would solve most of its problems. In the meantime, Dorsey may have to settle for helping the nearby barista sell a few more cups of coffee. And maybe that isn't such a bad fate after all.

how to find the perimeter of a square

Source: https://www.fastcompany.com/3033412/back-to-square-one

Posted by: petersonhinse1964.blogspot.com

0 Response to "how to find the perimeter of a square"

Post a Comment